Chinese Steel Market Highlights - Week 22, 2019

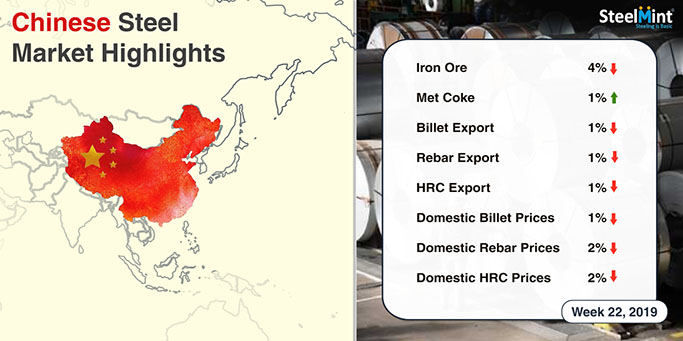

This week Chinese steel prices witness pessimistic market sentiments over increased supply and weakening prices in domestic market. However spot iron ore prices reported decline by the end of this week.

Meanwhile Chinese HRC and rebar export offers also remained downside. Coking coal offers inch down further. Iron ore prices rebounded towards the end of this week. However billet export offers reported marginal decline over bearish sentiments in China.

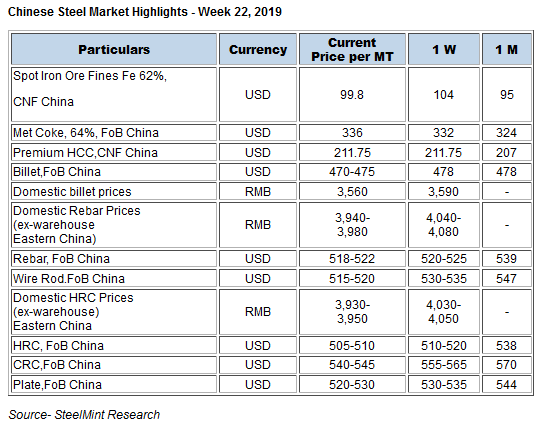

Chinese spot iron ore prices rebound towards the weekend- Chinese spot iron ore prices opened up this week at USD 108/MT, CFR China and dropped to USD 99.8/MT towards the weekend. The prices towards beginning of the week stood five years high amid supply concerns from Vale over expectation of dam rupture. However, during this week the prices fell amid Vale announcement of lower risk at collapsing of Gongo Soco mining pit.

Iron ore inventory at major Chinese ports dropped W-o-W to USD 124.9/MT,CFR China against USD 127.8/MT,CFR China a week ago.

Spot lump premium witnessed rise to USD 0.3400/DMTU,CFR China as against USD 0.3230/DMTU CFR China last week.

The prices have picked up amid tight supply and are expected to continue for the month of June.

Spot pellet premium picked up W-o-W-: Spot pellet premium for Fe 65% grade pellets picked up to USD 27.30/DMT,CFR China this week as against USD 23.20/DMT, CFR China towards last week due to limited offers in spot market. Preference for pellet is more compared to lump due to hike in coke prices. However, the pellet port inventory at major Chinese port still remains at 5 MnT.

Coking coal offers weaken further- Seaborne premium hard metallurgical coal prices witness decline on weekly basis amid lackluster demand from steel mills in China.

Most of the buyers in China have kept themselves away citing current price levels. However in the Indian market, spot demand for July-August-loading cargoes of imported coking coal has now moderated, due to an approaching monsoon.

Latest offers for the Premium HCC grade are assessed at around USD 203.50/MT FOB Australia. Previous week the offer was hovering at USD 205.50/MT FoB basis.

Chinese billet prices increase on weekly basis- This week Chinese domestic billet prices settled at RMB 3,560/MT, down RMB 30 against last week. This week, billet trade sentiments in China reported weak.

Chinese HRC export offers fell further over ample supply- Chinese HRC export offers witness slump this week owing to volatile futures and falling steel prices in domestic market. Meanwhile higher levels of inventory in domestic market also weigh on Chinese steel prices.

Also intensifying trade tensions between USA and China on implementation of hike in tariffs from 10% to 25% on various products from 1st June’19 has put pressure on steel prices in China.

Thus currently nation’s HRC export offer declined by USD 5-10/MT and was assessed at around USD 500-505/MT FoB basis.In the beginning of the week offers stood at USD 510-520/MT FoB basis.

Meanwhile domestic HRC prices in China is hovering at RMB 3,990-4,000/MT fell by RMB40/MT W-o-W basis against RMB 4,030-4,050 /MT in eastern China (Shanghai).

And prices at Northern China fell by RMB 50/MT and stood at RMB 3,960-3970/MT against RMB 3,910-3,920/MT in Northern China (Tangshan).

Chinese rebar export offers inch down over weakening domestic prices- Nation’s rebar export offers fell this week owing to falling rebar prices in domestic market.

Currently nation’s rebar export offers are at USD 522/MT FoB China. Last week the offers were at USD 525-530/MT FoB basis.

However domestic rebar prices stood at RMB 3,990-4,030/MT (Eastern China) fell by RMB 50/MT W-o-W against previous week.However prices which stood at RMB 4,040-4,080/MT inclusive of VAT taxes.

source: SteelMint

Top News