Chinese Steel Market Highlights Week-23, 2019

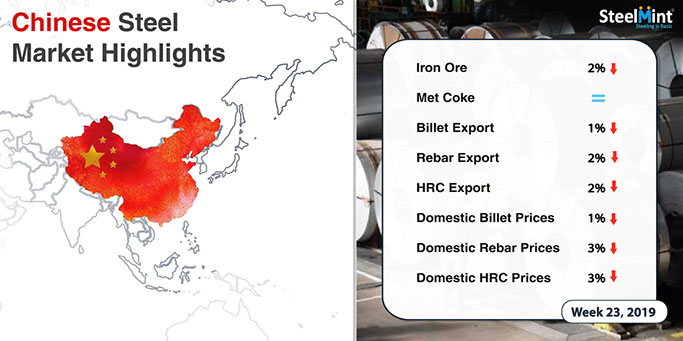

This week Chinese steel prices reported continual decline and witnessed significant fall amid pessimistic market sentiments and dull outlook prevailing in domestic market. Also volatile futures lead to further fall in steel prices in China.

Weakening domestic steel prices kept nation’s export offers on declining mode. Chinese HRC and rebar export offers continued to remain downside. Coking coal offers inched down further. Iron ore prices reported fall. Although billet export offers remained largely stable.

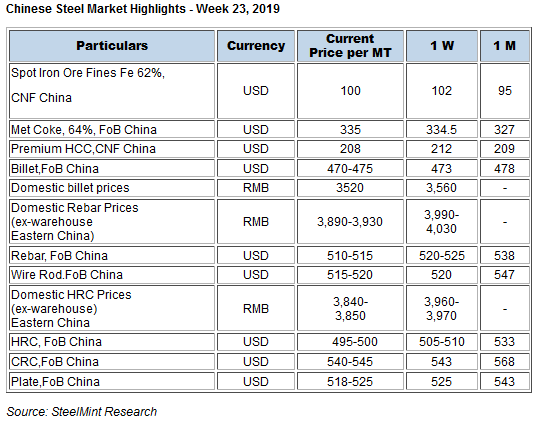

Chinese spot iron ore prices fell on weekly basis - Chinese spot iron ore prices dropped this week after hitting five years high at USD 108/MT towards last week. The prices softened amidst easing supply concerns from Vale. Also, Vale announced resumption of freight train operation on the Belo Horizonte branch line this week amid reduced risk from movement in Gongo Soco mines.

Spot lump premium witnessed drop to USD 0.33/DMTU, CFR China as against USD 0.3400/DMTU, CFR China last week. However, the prices are expected to rise for the month of June amid tight supply.

Spot pellet premium picked up amid decline in global iron ore price- Spot pellet premium for Fe 65% grade pellets assessed at USD 28.15/DMT, CFR China this week, up by USD 0.85/DMT W-o-W against USD 27.3/DMT a week before.

Coking coal offers inch down- Seaborne premium low-volatile hard coking coal prices have remained on downward trend amid softening overseas demand.

Traders are trying to clear previous stock available before prices fall further amid ample supply.

Meanwhile Indian importers are actively seeking for Australian coking coal in order to replenish their inventories ahead of monsoon season.

Latest offers for the Premium HCC grade are assessed at around USD 202.50/MT FOB Australia, which was USD 205.50/MT FOB Australia previous week.

China domestic billet prices decline further- This week Chinese domestic billet prices settled at RMB 3,520/MT, down RMB 40 against last week and trade sentiments in China reported weak.

Chinese HRC export offers witness continual decline- Chinese HRC export offers witness continual decline since the beginning of the week following pessimism in domestic market.

Thus currently nation’s HRC export offers are assessed at USD 495-500/MT FoB basis which was USD 505-510/MT FoB basis. On weekly basis nation's HRC offers fell by USD 10/MT.

Thus ample supply and slump in buying activities lead to significant fall in Chinese steel prices. Also China observed holiday yesterday on the occasion of Dragon Boat festival which kept HRC prices on lower side in domestic market.

Meanwhile domestic HRC prices in China is hovering at RMB 3,840-3,850/MT fell significantly by by RMB 120/MT W-o-W basis against RMB 3,960-3,970 /MT in eastern China (Shanghai).

And prices at Northern China (Tangshan) fell by RMB 80/MT and stood at RMB 3,790-3,800/MT against RMB 3,870-3,890/MT in Northern China (Tangshan).

End users are postponing their purchases amid bearish market outlook both in domestic and export market.

Chinese rebar export offers fell further- Nation’s rebar export offers reported further decline by USD 10-15 /MT owing to weakening sentiments in domestic market.

Bearish market sentiments along with public holiday on the occasion of Dragon Boat festival reported further slump in prices.

Currently nation’s rebar export offers are at USD 510-515/MT FoB China. Last week the offers were at USD 520-525/MT FoB basis.

Meanwhile domestic rebar prices stood at RMB 3,890-3,930/MT (Eastern China) fell by RMB 100/MT W-o-W against previous week. Previous week prices stood at RMB 3,990-4,030/MT inclusive of VAT taxes.

source: SteelMint

Related News

Top News