Chinese Steel Market Highlights- Week 39, 2019

This week Chinese finished steel prices continued to remain volatile amid fluctuations in the futures market. With the aspiration of clear and pollution-free sky, stringent production curbs announced by Hebei, Shanxi and Shandong provincial govt ahead of China’s National Day processions on 1st Oct’19 sent spot steel prices soaring. However, prices could not sustain the momentum and started to decline towards the end of the week with the curbs engrossing major downstream steel-consuming sectors resulting in a decline in demand.

China’s HRC export offers fell however, rebar export offers remained largely supported ahead of Golden Week holidays. Iron ore prices remained firm on a weekly basis. However, billet export offers witnessed a marginal decline.

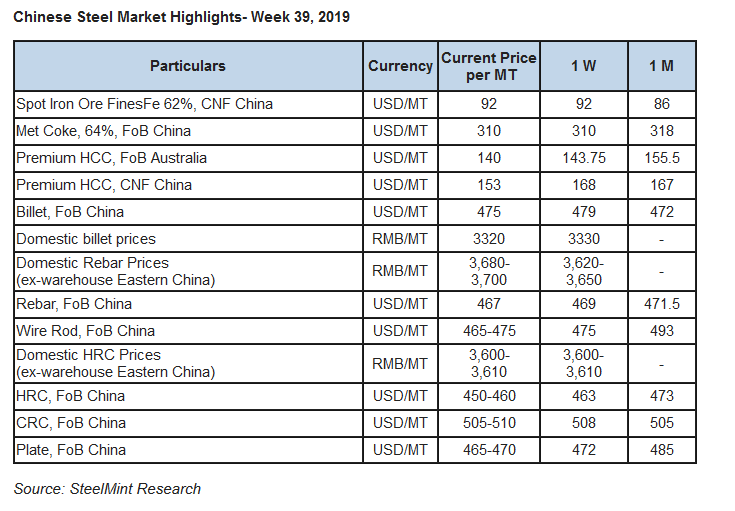

Chinese spot iron ore remains unchanged on a weekly basis- Chinese spot iron ore prices opened up this week at USD 93.65/MT, CFR China and dropped to USD 91.5/MT, CFR China towards the weekend similar to the prices in the previous week. Prices have dropped down amid rising port stocks.

As per data compiled by SteelHome consultancy, Iron ore inventory at major Chinese ports increased to 125.55 MnT as compared to 124.1 MnT a week ago.

Spot pellet premium up W-o-W- Spot pellet premium for Fe 65% grade pellets assessed at USD 17.05/MT, CFR China as against USD 12.15/MT, CFR China a week before.

Pellet premium has witnessed rise after production curbs announced in China.

Spot lump premium remains firm on a weekly basis- Spot lump premium picked up on a weekly basis to USD 0.1450/DMTU as against USD 0.1260/DMTU assessed last week. The rise is due to recovery in lump demand by Chinese mills.

Coking coal offers slide further on a weekly basis- Seaborne hard coking coal prices plummeted this week, amid an oversupply of lower quality seaborne cargoes and import restrictions in Chinese ports. However, traders remain concerned about further drop in demand with the import quotas nearly exhausted at ports.

In India, the demand has been dampened by the prevailing bearishness in the domestic steel sector.

The latest offers for the Premium HCC grade are assessed at around USD 137.00/MT FoB fell by USD 6.75/MT W-o-W basis which was USD 143.75/MT FoB basis in the previous week.

Chinese domestic billet prices slide further- Yesterday the billet price in Tangshan, Changli, and QIan'an was settled at RMB 3,320 ex-factory, including tax. Today the Changli area saw price uptick by RMB 20/MT to RMB 3,340/MT. Most finished steel prices tend up with some resources stabilized.

Chinese HRC export offers declined amid increased overseas competition- This week Chinese HRC export offers witnessed a decline of around USD 10/MT as low priced imports to Vietnam from India and Russia keep weighing on the Chinese origin HRC offers.

Currently, the nation’s HRC export offers are hovering at USD 450-460/MT, FoB as against USD 460-465/MT in the previous week.

Domestic HRC prices kept hovering at RMB 3,600-3,610/MT in Eastern China (Shanghai).

Chinese Rebar export offers remain supported on a weekly basis- This week Chinese rebar export offers remained largely stable amid restocking in the domestic market ahead of the Golden Week holidays.

However, overseas buyers stick to the wait and watch approach in anticipation of lower offers from Chinese mills.

Currently, the nation’s rebar export offers stood at USD 465-470/MT FoB China which was USD 464-474/MT FoB China in the previous week.

Meanwhile, domestic rebar prices stood at RMB 3,680-3,700/MT (Eastern China) as against RMB 3,620-3,650/MT (Eastern China) a week ago.

source: SteelMint

Top News