China: Higher bidding prices of Chrome Ore failed to drive the Chrome ore and Ferro Chrome market

In October, China's chrome ore market did not show any positive trend. Importers neither have the intention to import cargo nor do they want to speculate on spot goods. Hence, the market showed no major adjustments.

Due to the big volume of inventory of RSA cargo at the port, most factories have sufficient in-plant stock and their procurement enthusiasm dwindles because of recent intensified new cargo arrivals at the port. Considering this, a few traders have adjusted their sales tactic to turn down offer levels in a limited scope though.

The procurement of chrome ore both from overseas suppliers and port source in China are at low tide. At present, most factories order their cargo directly from overseas suppliers and domestic procurement are mainly focusing on replenishing needs or small parcels from the domestic port, leading to sluggish performance at most of the Chinese ports. While the new arrivals at the port are intensified recently, most factories are still on consuming own inventory. Those factories that are mainly taking port cargos also have no intention in building up stock, they are only taking small amounts in a short period instead. Some users take to demand lower prices after a period of waiting stance but so far no consensus reached between buyers and sellers on price. However, the high positioned offer used to appear previously no longer exists, and it is likely that traders will compromise on price through the wiggling room is not much.

The mainstream transaction price of general Si content high-chromium (50-basis ex-factory including tax):

Southwest China RMB6,450-6,500; Northwest RMB6,450-6,500; Northeast 6,750-6,850; East China 6,650-6,700; Central China 6,500-6,600; North China 6,350-6,400.

Low-silicon (silicon content less than 1.5) high-carbon ferrochrome mainstream ex-factory tax-including price at RMB7, 050-7,100 / 50 basis tons; ex-factory price of offers from distributors is mainly at RMB7, 100-7,200 / 50 basis per tons.

There is no adjustment for the price of high carbon ferrochrome last week. At present, HC ferrochrome transactions are stuck in an embarrassing situation. Traders admit that the recent downstream orders are scarce, so the main focus is on consuming previous inventory, and the purchasing interest is not high. Intermediaries working with large steel mills are reluctant to unilaterally bear losses from the low prices by steel mills and have to shift the pressure to the factory. Some factories suffered from capital strain are offering more flexibility on price as shown in Inner-Mongolia of the price at RMB6, 200-6,250/50 basis, cash including tax. But this offer is non-mainstream and the whole market is still dominated by waiting sentiments given that cost restraint leaves little room for big compromise by factories.

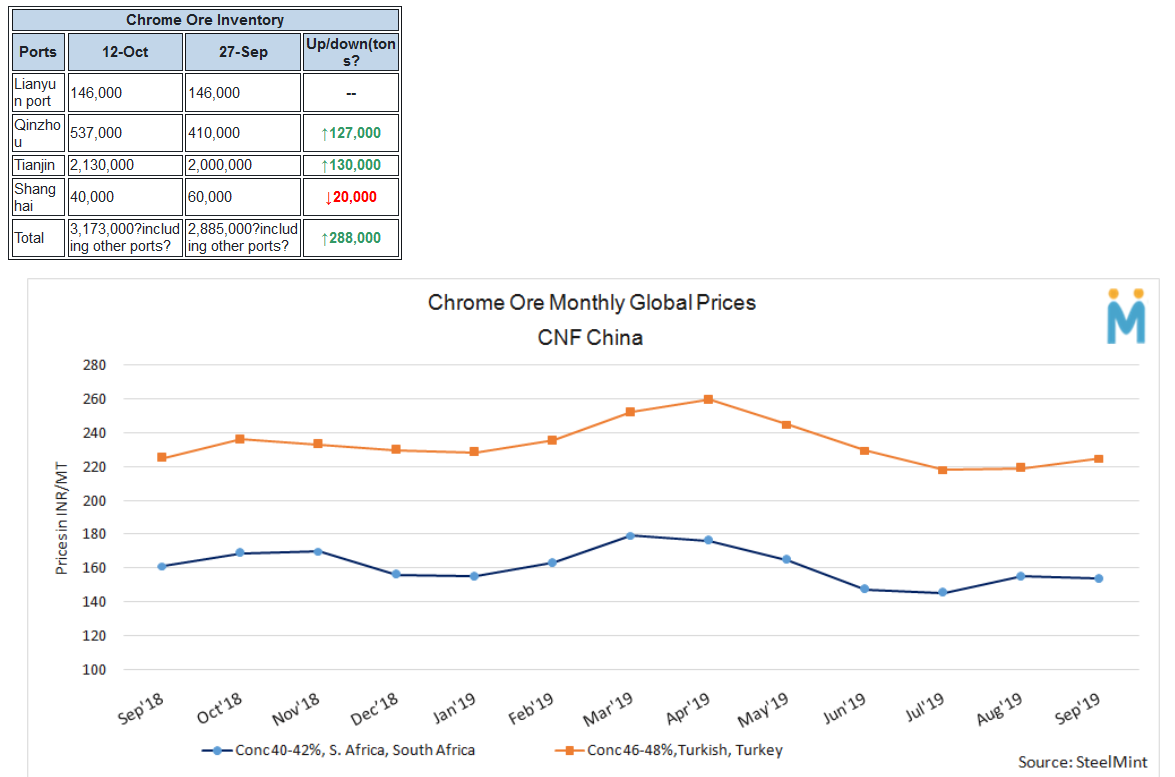

Up until last Saturday, the spot inventory of chrome ore at Chinese ports was 3.173 million tons, which was 288,000 tons more than that (2.885 million tons) on September 27. (The number of unpacked containers and those in bonded warehouses at Tianjin Port was not counted). During the National Day holiday, the chrome ore out-bound delivery was basically stagnant due to the fact that the chrome industry was at rest. Meanwhile, the arrivals of new cargo at the port have intensified recently, leading to a surge in port inventory to more than 3million tons.

source: SteelMint

Top News

twenty-one Minutes ago