Indian Steel Market Weekly Snapshot

Indian spot steel trades remained limited during the week-47 (16-23rd Nov'19). Participants mentioned that, inquiries were less than the average, however due to sufficient orders in hand, the producers have slightly change their offers.

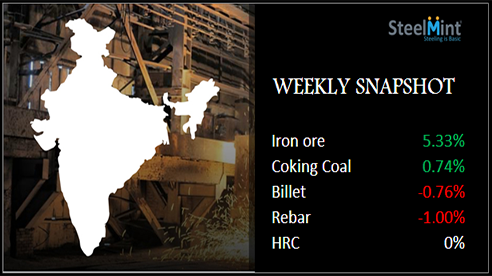

As per assessment made by SteelMint, this week prices of Semis & Finished long steel products have fluctuated by INR 100-400/MT (upto USD 6). Meanwhile, the domestic Flat steel prices more or less firm on weekly basis.

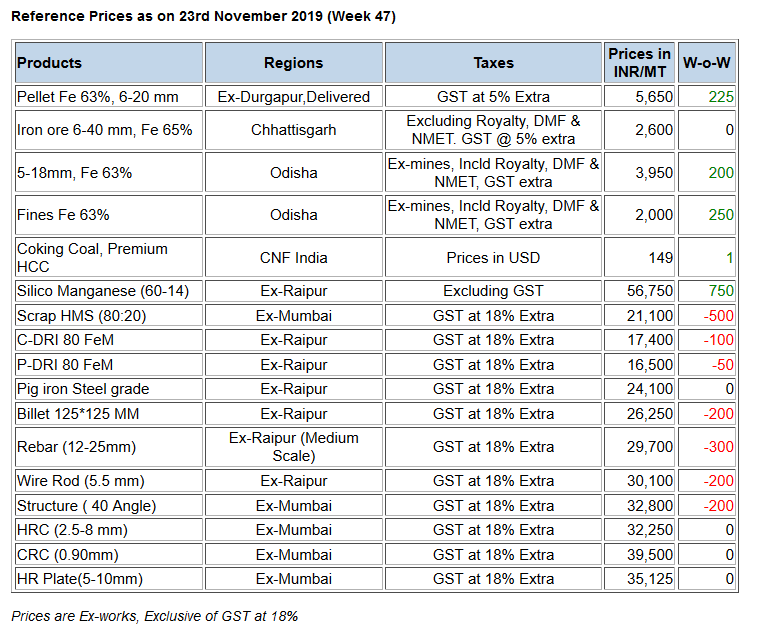

IRON ORE and PELLETS

Odisha's major merchant iron ore miners had increased iron ore lump offers for 5-18 mm (Fe 63%) by INR 300/MT. SteelMint assessment for 5-18 mm (Fe 63%) stands at INR 3,900-4,000/MT (ex-mines, including Royalty, DMF & NMET).

Odisha Mining Corporation (OMC) had scheduled an auction for sub-grade iron ore fines yesterday (i.e. on 22nd Sep'19). Total quantity put under the auction was 525,000 MT fines (Fe 56%). As per sources report to SteelMint, entire material got booked. Bids moved up by around INR 300-350/MT over the set base price of INR 500/MT (including Royalty). Bids received were at INR 800-850/MT.

-- PELLEX (DAP Raipur), 63.5% Fe this week increased by INR 100/MT to INR 6,200/wmt in recent deals. Raipur based pellet makers raised offers by INR 100-200/MT to INR 6,200-6,300/MT( Ex-plant).

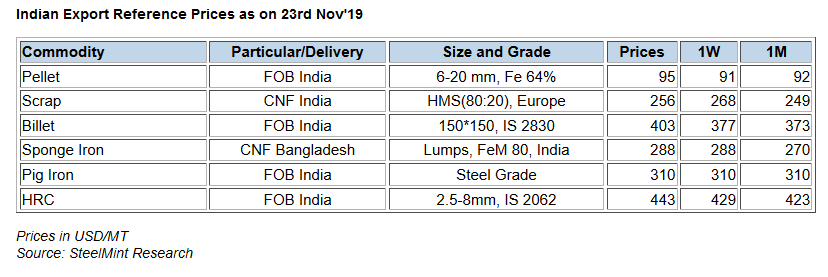

-- KIOCL has concluded pellet (low Al) export deal for 50,000 MT at around USD 98/MT, FoB India.

COAL

Australian premium low-volatile hard coking coal prices have remained rangebound this week, after having slipped down by USD 3/MT on Monday amid lower offers and fresh bookings concluded late last week in China.

The spot market saw increased trading activity, with Chinese end-users buying more seaborne cargoes, in hopes of utilizing their revamped import quotas in January 2020. Meanwhile, most of the market participants eagerly awaited results of ongoing negotiations for Chinese steelmakers’ annual long term contract prices and volumes with domestic coking coal miners.

-- Latest offers for the Premium HCC grade are assessed at around USD 133.00/MT FOB Australia and USD 146.40/MT CNF India.

FERROUS SCRAP

Limited trades for imported Scrap to India ensured the offers from global suppliers moving down significantly this week, in line with the trend in other South Asian markets.

-- SteelMint’s offers for containerized Shredded from the UK, Europe and the USA to India have come down to USD 280-284/MT, CFR Nhava Sheva, down by USD 8-10/MT against last week's report, while offers for P&S now stand at around 290/MT CFR Nhava Sheva.

-- Offers for South African origin hand loaded HMS 1 stood in the range of USD 265-270/MT CFR. UAE origin HMS offers also plummeted significantly against last week, with HMS 1 super (no ci gi) from Dubai standing in the range of USD 270-274/MT CFR.

-- West African HMS 1&2 (80:20) was reportedly sold at USD 260/MT CFR Goa this week. European and UK origin HMS 1&2 (80:20) was being offered at around USD 255-257/MT CFR.

FERRO ALLOY

-- Silico Manganese prices increased amid short supply in the market. Most of the producers are operating at a much lower capacity. Current assessment in Durgapur is at INR 57,000/MT whereas, in Raipur, prices are at INR 56,500-57,000/MT ex-plant.

-- Ferro Manganese prices are stable due to low supply in the domestic market. Prices are likely to increase amid less availability of material and ore prices firming.

-- Ferro Chrome prices fell significantly due to higher selling pressure and low demand in the domestic and overseas markets. Producers are aggressively trying to sell now as market anticipation is for further fall in Ferro Chrome prices.

-- Ferro Silicon prices in Bhutan and Guwahati are stable, as the supply-demand dynamics are comparatively balanced.

SEMI FINISHED

Indian Billet market observed volatility in prices by INR 100-400/MT due to subdued demand & adjusted production, specifically in central & western regions.

Further, as per producers in eastern India, demand was not upto the mark from the domestic buyers. Also, export inquiries were limited for both Sponge iron & Billet. Thus, sponge iron offers being fluctuates by INR 100-200/MT, W-o-W.

-- Indian sponge iron (80 FeM, 100% lumps) export offers hovering at USD 270-275/MT CPT Benapole, equivalent to USD 285-290/MT, CFR Chittagong, Bangladesh.

-- Indian large mills export offers to Nepal slightly increased & currently reported at around USD 410/MT for Billet & USD 455/MT for Wire rod, CPT Raxaul border.

-- SAIL has conducted auction from its central India based Bhilai Steel Plant (BSP) for defective billets on 15 Nov’19. The bids of billet were decreased by around INR 250-350/MT compared to the previous auction to INR 24,350-25,750/ MT (EXW-Bhilai).

-- Jindal Steel has kept steel grade pig iron offers firm at around INR 24,000/MT ex-plant, Raigarh. However as per officials, panther shots (granulated pig iron) is not available.

-- SAIL’s Rourkela Steel Plant auction held on 22nd Nov'19 to sell about 7,900 MT steel grade pig iron; has received average response. The base price for the auction was quoted by RSP at INR 23,050/MT, which is down by INR 450/MT (USD 6) as against previous auction and near about 50% material sold.

-- Tata Steel announced that its step-down subsidiary NatSteel Holdings Pte (NSH) has concluded sale of equity sales in NatSteel Vina (NSV) to a Vietnam based-steel making company Thai Hung Trading Joint Stock Company.

FINISH LONG

Indian Finish Long Steel market observed measured trade volume, as per weekly assessment. However according to market participants, slight improvement in demand would have been noticed from last couple of days in few locations and weekly rebar price range marked fluctuation of around INR 100-400/MT in overall major markets, except in northern India - Delhi, where it dropped by INR 800/MT due to ban construction activities in Nov'19.

Further, the trade participants are assuming that current market scenario of finish long steel is relatively sustainable with near average to trade volume as production level is not appropriate.

-- Current trade reference rebar prices (12-25 mm) through mid-sized mills assessed at INR 29,600-29,800/MT Ex-Raipur (central region) & INR 31,300-31,600/MT Ex-Jalna (western region).

-- Central region, Raipur based heavy structure manufacturers have maintained trade discount of INR 1,000-1,400/MT and Current trade reference prices registered at INR 33,400-33,800/MT (200 Angle) ex-work.

-- Trade discounts in Raipur wire rod is currently at INR 1,000-1,400/MT and trade reference prices stood at INR 29,600-30,100/MT ex-Raipur and INR 30,700-30,800/MT ex-Durgapur, size 5.5 mm.

FINISH FLAT

This week Indian HRC prices remained largely stable in major markets owing to sustained demand and improved sentiments in the domestic market. However in southern region price increased on a weekly basis.

As per SteelMint's price assessment, current trade reference prices in traders segment for HRC (IS2062, 2.5-8 mm) is at INR 35,000-35,500/MT ex-Mumbai, INR 34,500-35,000/MT ex-Delhi and INR 35,500-36,000/MT ex-Chennai. And the domestic CRC (0.9 mm, IS 513) trade reference prices on a weekly premise are hovering around INR 39,000-40,000/MT ex-Mumbai, INR 38,500- 39,000/MT ex-Delhi and INR 39,000-40,000/MT ex-Chennai. Prices mentioned above are basic, and extra GST@ 18% will be applicable.

Decent export bookings on higher offers and restocking activities post Diwali holidays propelled Indian steel mills to increase the prices in the beginning of Nov'19.

Indian HRC export offers to Vietnam - Indian steel mills recently booked 5,000-10,000 MT of HRC for exports to Vietnam at USD 450-455/MT CFR basis for Dec end- Jan shipments. Last week the offer was in the range of USD 440-442/MT CFR Vietnam.

source: SteelMint

Top News