Chinese Steel Market Highlights- Week 47, 2019

This week nation's domestic steel prices reported a surge on a weekly basis over restricted supply amid recently announced production curbs. Along with this, RMB strengthening over USD, and strong domestic demand resulted in an upside in steel prices.

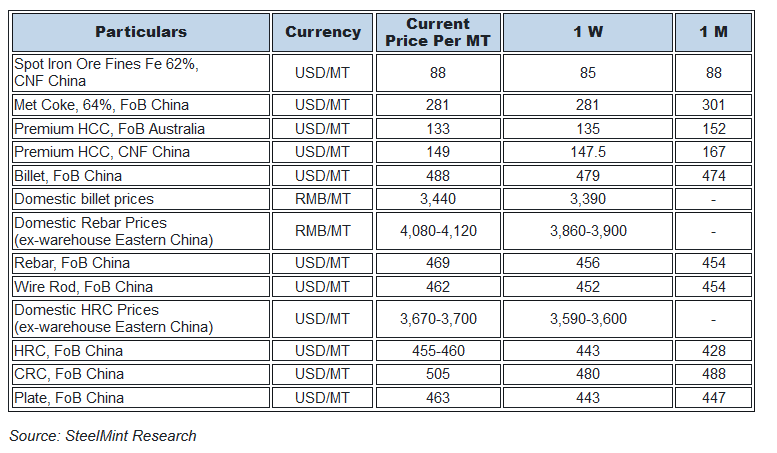

Meanwhile, the nation's HRC and Rebar export offers rose amid strong demand over restocking activities ahead of the New Year holidays. Iron ore prices picked up amid falling inventories at Chinese ports. However, coking coal prices declined this week. Meanwhile billet export offers also witness uptick on a weekly basis.

Chinese spot iron ore prices up during the week- Chinese spot iron ore prices opened up this week at USD 85.10/MT, CFR China and increased to USD 87.80/MT, CFR China towards the weekend. The prices were supported due to failing inventories at major Chinese ports.

As per data compiled by SteelHome consultancy, Iron ore inventory at major Chinese ports dropped to 129.5 MnT as against 130.35 MnT assessed towards the end of last week.

Spot pellet premium down 23% W-o-W- Spot pellet premium for Fe 65% grade pellets dropped sharply to USD 20.85/DMT, CFR China as against USD 27.05/DMT, CFR China assessed last week. The pellet premium has witnessed a fall amid rising fines prices.

The pellet market is expected to remain supported due to stringent environmental controls, higher steel margins and falling port inventories.

As per data compiled by SteelHome consultancy, Pellet inventories were reported at 6.5 MnT this week against 6.9 MnT towards last weekend.

Spot lump premium down W-o-W- Spot lump premium this week dropped to USD 0.2100/DMTU as against USD 0.2145/DMTU towards last week. Amid sintering cuts, demand for lumps remain supported.

Coking coal prices inch down on a weekly premise- This week, the seaborne coking coal prices slipped down by $3/MT amid market participants awaiting the results of ongoing negotiations for Chinese steelmakers' annual long term contract prices and volumes with domestic coking coal miners.

The latest offers for the Premium HCC grade assessed at around USD 133.00/MT FOB Australia and USD 136/MT FoB basis in the previous week.

China’s billet prices surge over strong demand- The nation’s domestic billet market was settled at RMB 3,440/MT, up RMB 50/MT as against RMB 3, 390/MT a week ago. The market sentiments in the country are strong in the country. Meanwhile, the nation's billet export offers moved up by USD 5/MT on a weekly basis.

China HRC export offers witness surge over scant supply- This week, Chinese HRC export offers reported an increase of around USD 15/MT on a weekly basis.

Lower HRC supplies owing to recently announced production curbs led to an increase in the domestic and export prices this week. Meanwhile, traders in the domestic market are actively restocking the material ahead of the New Year holidays.

Thus, current Chinese HRC export offers stand at USD 455-460/MT FoB China in contrast with USD 440-455/MT FoB basis at the beginning of the week.

Meanwhile, domestic HRC offers surged by RMB 80-100/MT, to RMB 3,670-3,700/MT, as compared to RMB 3,590-3,600/MT in the preceding week.

China Rebar export offers move up W-o-W- This week the Chinese rebar offers increased by USD 10/MT on the back of robust demand in the domestic market ahead of the falling temperatures in the Dec month.

Thus, current Rebar offers stand at USD 465-470/MT FoB China as compared to USD 455-460/MT FoB basis a week ago.

Meanwhile, domestic Rebar offers spiked by RMB 220/MT, to RMB 4,080-4,120/MT, as compared to RMB 3,860-3,900/MT in the preceding week.

source: SteelMint

Top News